Draft Income Tax Rules 2026: Key Changes in PAN, HRA and Allowances Explained

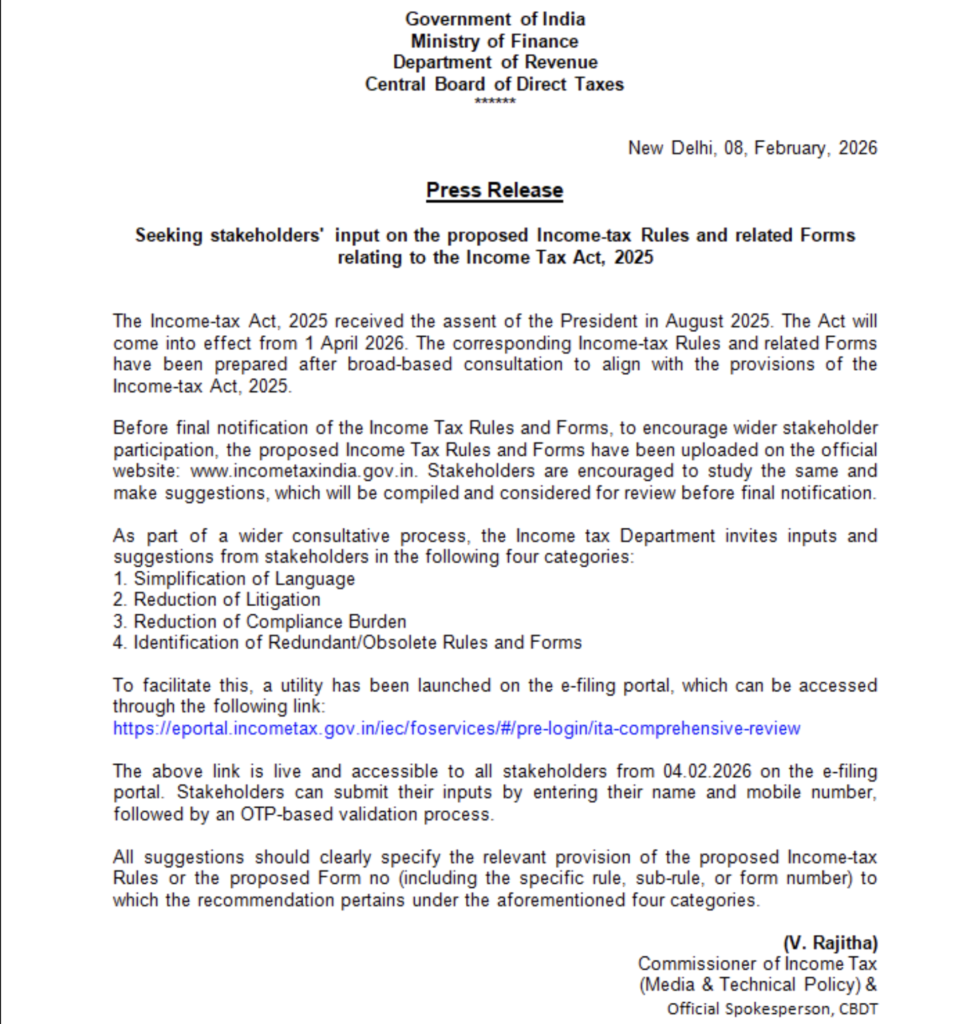

The draft Income tax Rules 2026 released by the Central Board of Direct Taxes (CBDT) provide the clearest picture yet of how the Income-tax Act, 2025 will function when it comes into force from April 1, 2026. The proposed rules introduce significant changes affecting everyday financial transactions, salary structures, tax reporting and compliance requirements.

While several provisions aim to ease compliance for ordinary taxpayers by raising thresholds and updating outdated exemptions, the framework also strengthens reporting and scrutiny in areas involving high-value transactions, insurance investments, rental income and cross-border taxation. The draft rules are currently open for public feedback before final notification.

Key Highlights of Draft Income Tax Rules 2026 and Their Impact on Taxpayers

- PAN quoting thresholds proposed to be significantly increased for cash transactions, property purchases and hospitality payments.

- Higher tax-free limits for employer-provided meals, gifts, education allowance and staff loans.

- Revised valuation of employer-provided cars expected to increase taxable salary for some employees.

- Expansion of higher HRA exemption to more cities including Bengaluru, Hyderabad, Pune and Ahmedabad.

- Fixed deposit reporting norms aligned with existing high-value transaction monitoring.

- Stronger digital compliance through enhanced reporting, pre-filled forms and technology-based scrutiny.

- Draft rules signal continued relevance of the old tax regime for salaried taxpayers claiming deductions.

PAN Rules Relaxed for Routine Transactions, Tightened for Insurance and Reporting

One of the most notable changes proposed under the draft rules is the revision of thresholds for quoting a Permanent Account Number (PAN). Under current rules, PAN is required for cash deposits exceeding ₹50,000 in a single day. The draft rules propose that PAN will be required only when total cash deposits or withdrawals across one or more accounts aggregate to ₹10 lakh or more in a financial year.

Similarly, payments made at hotels, restaurants, banquet halls or event management venues will require PAN only if the transaction exceeds ₹1 lakh, compared with the earlier ₹50,000 threshold. For motor vehicle purchases, PAN will be mandatory only if the transaction value exceeds ₹5 lakh, easing compliance for lower-value purchases.

Property transactions also see a higher threshold, with PAN required only when the value exceeds ₹20 lakh instead of ₹10 lakh earlier. However, insurance transactions move in the opposite direction, as PAN is proposed to be mandatory for all life insurance premium payments, strengthening monitoring of insurance-linked investments. ULIP maturity proceeds will continue to be taxable where annual premiums exceed ₹2.5 lakh.

Employer Perquisites and Salary Structure Changes

The draft rules revise the valuation of several employer-provided benefits. The taxable value of employer-provided motor cars has been increased significantly to reflect current market realities. For cars with engine capacity up to 1.6 litres, the taxable perquisite value is proposed at ₹8,000 per month, while cars with higher engine capacity will attract a valuation of ₹10,000 per month.

At the same time, several exemptions have been liberalised. The tax-free limit for employer-provided meals has been increased from ₹50 to ₹200 per meal, while the exemption for gifts or vouchers from employers is proposed to rise from ₹5,000 to ₹15,000 annually. Interest-free loans from employers are proposed to be tax-free up to ₹2 lakh, compared with the earlier limit of ₹20,000.

These changes allow employers greater flexibility in structuring compensation while increasing the non-taxable component of salary in certain cases.

Also Read: Fundamental Tax-Saving Provisions: How To Save Tax Legally in India?

Education Allowances, Hostel Benefits and HRA Expansion Offer Relief to Families

A major relief under the draft rules comes in the form of increased education-related exemptions. The children’s education allowance is proposed to increase from ₹100 per month per child to ₹3,000 per month per child. Similarly, the hostel expenditure allowance is proposed to rise from ₹300 to ₹9,000 per month per child.

The list of cities eligible for the higher 50 percent House Rent Allowance exemption has also been expanded. Bengaluru, Hyderabad, Pune and Ahmedabad are proposed to be included alongside Delhi, Mumbai, Kolkata and Chennai. This change is expected to significantly reduce taxable income for salaried individuals living in high-rent urban centres under the old tax regime.

Fixed Deposits, High-Value Transactions and Reporting Requirements

The draft rules also clarify reporting requirements for high-value transactions. Banks and post offices will be required to report new fixed deposits aggregating to ₹10 lakh or more in a financial year to the Income-tax Department. Renewals of existing fixed deposits will not be covered under this reporting requirement.

Cash deposits aggregating to ₹10 lakh or more in a financial year in one or more accounts will continue to be reportable for PAN holders, while the threshold for non-PAN holders remains ₹5 lakh. These provisions largely continue the existing framework under earlier rules but align them with the new law.

In addition, crypto-asset service providers will be required to share transaction information with tax authorities, and Central Bank Digital Currency has been recognised as an accepted electronic payment mode.

Simplified Compliance, Digital Processing and Structural Changes Under the New Law

The draft rules introduce a more technology-driven compliance framework. Standardised information across forms, pre-filled data and automated reconciliation are intended to reduce errors and simplify filing. A digital-first approach to notices and communication is expected to improve efficiency in tax administration.

The Income-tax Act, 2025 itself reorganises and renumbers several sections without fundamentally altering the underlying principles of taxation. The new framework reduces the number of rules and forms and aims to provide a clearer structure. Rental income, however, is expected to face closer scrutiny through improved data matching and reporting integration.

For individuals claiming Foreign Tax Credit, certification by a Chartered Accountant will be mandatory where foreign tax paid exceeds ₹1 lakh.

Spiritual Perspective: True Knowledge and Righteous Living in the Teachings of Saint Rampal Ji Maharaj Ji

Beyond financial reforms and changing tax structures, spiritual wisdom reminds individuals that material systems alone cannot bring lasting peace or satisfaction. The teachings of Saint Rampal Ji Maharaj emphasise living a truthful, ethical and disciplined life while earning through honest means and avoiding exploitation or greed.

His spiritual knowledge explains that true prosperity lies in balanced living, where worldly responsibilities are fulfilled with righteousness and spiritual awareness. Such guidance encourages individuals to remain morally conscious in financial dealings, promoting honesty, simplicity and inner peace alongside material progress.

How the Draft Rules Could Influence Tax Choices Going Forward

The proposed increase in exemptions and allowances available only under the old tax regime may influence tax planning decisions, particularly for salaried individuals with higher deductions. Enhanced HRA benefits, education allowances and employer-related exemptions may make the old regime more competitive for certain income groups, while the new regime may continue to remain attractive for taxpayers with fewer deductions.

Taken together, the draft Income-tax Rules, 2026 reflect a policy approach that seeks to reduce friction in everyday transactions while strengthening oversight of high-value and digitally traceable financial activities. With the rules currently open for public consultation, taxpayers and industry stakeholders now await the final notification before the new framework comes into effect from April 2026.

FAQs on Draft Income Tax Rules 2026 and Income Tax Act 2025 Changes

1. When will the Draft Income Tax Rules 2026 come into effect?

The Draft Income Tax Rules 2026 are proposed to come into effect from April 1, 2026, along with the implementation of the Income Tax Act, 2025 after final notification.

2. What is the new PAN requirement limit under Draft Income Tax Rules 2026?

PAN will be required only when cash deposits or withdrawals exceed ₹10 lakh annually, hotel payments exceed ₹1 lakh, or property transactions exceed ₹20 lakh.

3. How will Draft Income Tax Rules 2026 impact salaried employees?

The rules increase tax-free limits for meals, gifts, education allowance and HRA benefits, while revising taxable valuation of employer-provided cars and certain perquisites.

4. Will fixed deposits be reported to the Income Tax Department under new rules?

Banks must report new fixed deposits aggregating ₹10 lakh or more in a financial year, excluding renewals, under reporting requirements of the draft rules.

5. Will the old tax regime become beneficial after Draft Income Tax Rules 2026?

Higher exemptions like HRA, education and hostel allowances may make the old tax regime beneficial for salaried taxpayers claiming significant deductions compared to the new regime.

Related Stories

Discussion (0)