The Real Cost of ‘Buy Now, Pay Later’ Schemes

‘Buy Now, Pay Later’ (BNPL) schemes have emerged as a tempting solution for consumers in an era of instant gratification. Several payment platforms promote the idea of seamless purchases without immediate payment today, even to the extent of offering to split costs into interest-free instalments. This article examines the implications of ‘Buy Now, Pay Later’ schemes, analysing this global trend that has now set a firm foot in India too.

The Allure of Affordability

The ‘Buy Now, Pay Later’ scheme may seem like a financial blessing on the surface, more so for those looking to stretch their finances during the current economic uncertainty. However, behind the polished advertising is a growing concern – are BNPL schemes helping people manage their money, or pushing them further into financial instability?

Some points to note:

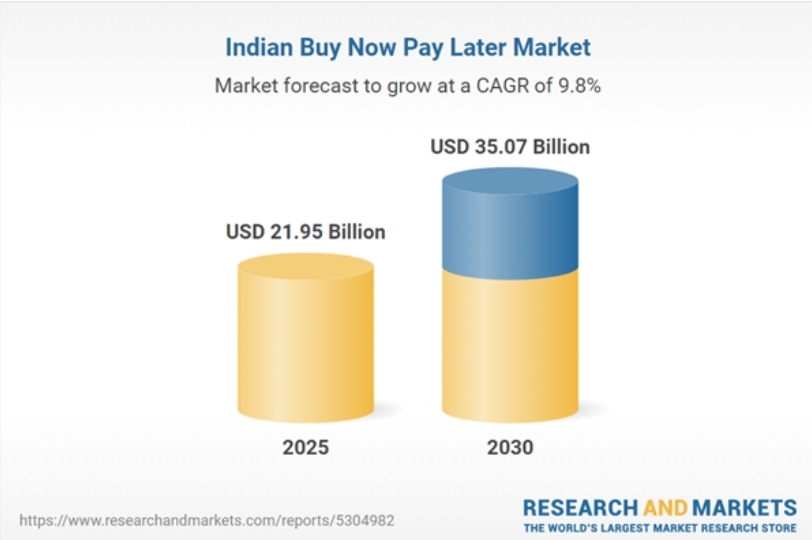

- According to a Global News Wire, BNPL usage in India will reach USD 21.95 billion by the end of this year 2025, further increasing to USD 35.07 billion.

Image Credit: Research and Markets

- BNPL schemes thrive on the psychology of affordability.

- Let’s study the example of a smartphone: A smartphone priced at INR 25,000 suddenly seems accessible when offered at INR 5,000 a month for five months. Similarly, for a person within a higher income bracket, a smartphone priced at INR 1,00,000 may seem affordable when offered at around INR 8,333 per month for a year.

- This approach often leads younger generations, particularly millennials and Gen Z, to make spontaneous purchases they might otherwise avoid.

- Majority of the target group are first-time credit users with little financial discipline or savings.

Are There Any Benefits?

For financially disciplined individuals, it can be a helpful tool for cash flow management, especially when dealing with big-ticket purchases or during emergencies. BNPL also opens up formal credit access to many Indians who were previously excluded from the banking system, such as students or entry-level professionals.

The Hidden Debt Trap

Though often marketed as interest-free, BNPL schemes come with their own risks. Late payments invite penalties and also being hounded by recovery agents. Frequent defaults can also negatively impact a user’s credit score. Many of these services do not clearly explain the long-term implications of missing payments, especially in India, where financial literacy remains low.

Defaulting even on very small amounts can affect an individual’s CIBIL score drastically. This affects one’s future loan and credit card eligibility in turn. Since many BNPL companies now report to credit bureaus, missing even small payments can have serious long-term consequences.

What makes BNPL even riskier than traditional credit cards is its ease of access. Most platforms offer instant approval with minimal KYC, and often without credit checks. This leads to overspending by those who may already be financially strained.

Paycheck-to-Paycheck Living: A Modern Reality

A worrying outcome of overreliance on BNPL is the reinforcement of paycheck-to-paycheck living. Earlier, this phenomenon was seen only in western countries. However, with the rising popularity of BNPL schemes and credit card culture, paycheck-to-paycheck living is increasingly visible in Indian metros too.

With easy EMIs and multiple credit lines, users end up committing their future income towards past purchases. Many a times these purchases are also just for instant gratification or even to reduce buyer’s remorse, which is more an illusion than a reality in case of BNPL schemes. As a result, there is little left for essentials, emergencies or savings.

BNPL schemes versus Credit Cards

There are some key differences between BNPL schemes and credit cards, and can be understood in the videos along with the table below:

| Aspect | BNPL schemes | Credit Cards |

| Approval | Easier to get approval as BNPL companies do not perform as many stringent checks as other financial lending companies. | Comparatively tougher to get approvals as credit card firms do a thorough financial check before approving the credit-worthiness of an applicant. |

| Interest charges | Typically, do not charge interest unless payments are defaulted on. | Credit card companies do have high interest rates that can even go upto 20-22% |

| Credit limit | BNPL lenders typically can lend upto INR 1,00,000 | Limit is set based on the screening process of the applicant that accesses their credit-worthiness |

| Repayment cycle | Varies from lender to lender, but is usually 14 to 30 days and can extend to 60-90 days. | Again, varies from lender to lender, but on an average, the lending cycle varies from 20 to 90 days. |

| Fees | Most often there is no joining fees | Some credit cards, especially the ones of higher financial tier do have yearly fees. |

| User Base | Wider user base as there are lesser restrictions. | A relatively limited number of users, as access is restricted by a thorough verification process. |

Regulation and Consumer Awareness

The Reserve Bank of India (RBI) has started paying attention to the growing influence of BNPL services. In 2022 and again in 2023, the RBI issued advisories and circulars aimed at clarifying the regulatory framework around digital lending.

However, enforcement is still evolving, and many BNPL players operate in grey areas without full accountability. In a statement made in December 2024, RBI Deputy Governor Michael Debabrata Patra highlighted that BNPL schemes and credit card usage encourage immediate consumption patterns, which in turn are diminishing the saving tendencies of the younger population.

Are You Selling Peace Instead of Buying Time? Choose a Foolproof Escape Through True Worship

BNPL schemes exploit human desires by offering instant gratification without immediate consequence. People fall into debt chasing temporary pleasures like gadgets, fashion, luxury, home, cars, etc. They believe it will bring happiness. Jagatguru Tatvdarshi Sant Rampal Ji Maharaj teaches that true happiness cannot be found in material objects, it can only be found in true spiritual knowledge bestowed by a Tatvdarshi Sant (Complete Saint).

Sant Rampal Ji Maharaj is the only True Saint in this world today, qualifying each prerequisite of being a Tatvdarshi Sant as mentioned in the Holy Vedas and the Holy Bhagavad Gita. The worship bestowed by Sant Rampal Ji is so powerful that it not only leads devotees to complete salvation, helping them break free from the vicious cycle of life and death, but also provides materialistic benefits as an effortless by-product of this true worship of Supreme God Kabir, the Ultimate Creator.

Buy Now, Pay Later schemes reflect the spiritual void in modern life, wherein people search for joy in objects instead of in the Divine. However, Sant Rampal Ji Maharaj offers a lasting solution to this struggle. Not just a short-term escape, but complete freedom from desires, financial burdens, and inner dissatisfaction.

Learn more about the eye-opening spiritual knowledge of Sant Rampal Ji Maharaj on:

- Website: www.jagatgururampalji.org

- YouTube: Sant Rampal Ji Maharaj

- Facebook page: Spiritual Leader Saint Rampal Ji

- X Handle: @SaintRampalJiM

Related Stories

Discussion (0)